Fernanda Santos and Gustavo Pereira’s London mortgage went from $2,800 a month to $4,400 a month

Fernanda Santos and Gustavo Pereira of London, Ontario, knew in March 2022 that the housing market was way overpriced, but they felt pressured to buy a home, so they paid $730,000 for a three-bedroom house in the east end.

“Everyone told us to buy as soon as we could.” “It didn’t matter if we liked it or not; we should just buy and get into the market.” In an interview with CBC Radio show host Rebecca Zandbergen, Santos, who is 34, said:London Morning.

In 2019, the couple left Brazil to start a new life in Canada. Today, they have a variable-rate mortgage (currently 5.6%) on a house whose value has dropped by an estimated $150,000 and are paying $4,400 a month, which is $1,600 more than they had planned.

“That’s not what we had in mind,” Santos said. “It’s been our worst nightmare.”

Since the beginning of 2022, the Bank of Canada has raised interest rates eight times to try to stop inflation. The rate set by the central bank is now at 4.5 percent.

Also, prices for homes have gone down a lot since the couple bought theirs. In fact, the Canadian Real Estate Association (CREA) said this week that sales in January were the lowest for that month since 2009. They were down 37.1% from a year ago.

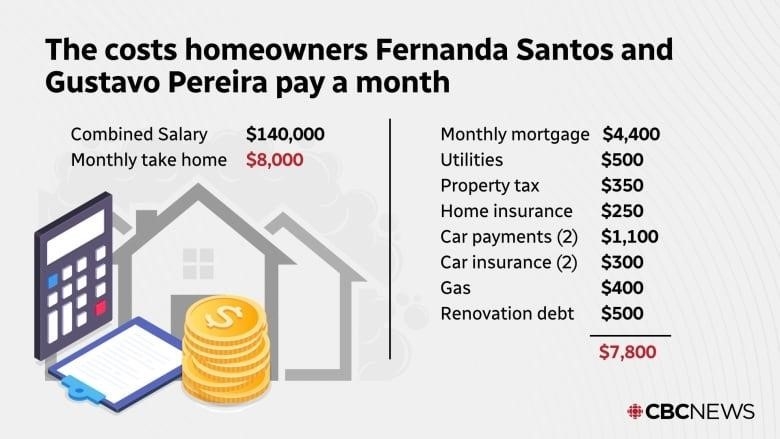

What Fernanda Santos and Gustavo Pereira’s books look like every month:

“They’ll just keep raising the rates until they’re happy with where they are,” Santos said. “But they don’t think about how that affects so many other people.”

Even though they both have good jobs and make a total of $140,000 a year between them, Santos and Pereira are having trouble keeping up. In Brazil, they both worked as engineers. Santos is now a senior estimator for a London construction company, and Pereira is learning to be an engineer.

“It’s not just the house payment,” Santos said. “We pay taxes on our property.” It’s a lot of money every month. We have insurance for both ourselves and the house. So there are many costs that aren’t obvious.

The couple also puts $500 a month toward fixing up their house.

The couple still has to work on the weekends. Both people drive for UberEats and Instacart to help pay their bills.

“When your mortgage takes up about 60% of your income, you don’t have much left to spend on other things, and we have to eat, right?” said Santos.

Santos and Pereira are also buying their groceries with money they have saved up for a rainy day.

Tips for homeowners who are feeling the squeez

John Pasalis, president and broker at Toronto’s Realosophy Realty Inc. and a housing analyst, said the couple should go back to their lender, RMG Mortgages, to see if they can negotiate a lower payment.

One option is to lengthen the amortization, which is how long it takes to pay off the mortgage in full. This can come with options for smaller monthly payments.

“I think people are reluctant to do that [negotiate], but they need to push,” said Pasalis, adding that lenders seem to be interested in “damping the shock” of rising mortgage payments right now.

Pasalis says that many people who have variable-rate mortgages are not actually paying more each month.

“When interest rates go up, most banks don’t really raise your payments on a variable mortgage,” he said. “Most of them have payments that don’t change.”

When this happens, more of a person’s mortgage payment goes toward interest and less toward the principal, which makes the mortgage last longer.

Santos and Pereira have put their plans to start a family on hold for the time being.

She said, “We had plans for the next few years, but I can’t take maternity leave right now.” “We won’t be able to pay our bills if I take maternity leave.”